Your Essential Economic & Stock Market Update (Q3 2022)

Everything You Need to Know About the Economy and the Stock Market Today

This event/webinar is purely educational and does not constitute as financial or investment advice. With investments, your capital is at risk. Investments can go down in value as well as up, so you could get back less than you invest.

📈Market updates can feel overwhelming and complex - but we love them here at Vestpod! That’s why we have prepared a no-nonsense, easy to understand quarterly economic and market update with Axelle Pinon, Equity Product Specialist Manager at Carmignac, and Emilie Bellet, Founder of Vestpod:

What’s happening with the stock market?

How does the economy impact your investments?

What has been driving the stock market over the past few months?

Macro insights on inflation, cost of living, spending and interest rates.

What we can expect going forward?

The aim of the session today is to provide an understanding of what is currently driving stock markets and consider the outlook.

I am really happy to introduce our brilliant partners for this session: Axelle, who is an Equity Product Specialist Manager at Carmignac. Carmignac is an independent asset management firm established in 1989 on three core principles that still stand true today: entrepreneurial spirit, human-driven insight and active commitment. The role of Carmignac is to enable their clients to improve their savings needs over the long-term.

The webinar was recorded on September 20th, 2022.

**Listen to the episode of The Wallet here via Podfollow.**

Key takeaways

While inflation and the cost of living are on everyone’s mind, it’s important to keep an eye on budgets and investments and to keep up with our investments, as there are likely to be great opportunities in the market for the long term.

Maybe it's the right time to also start looking more closely at what we are investing in. When you think about your investments - remember you’re investing in companies. It’s a great time to start looking more closely at those companies and how they make money. Look at the company's earnings and pay attention to actions from central banks.

Notice that some companies are more resilient than others when it comes to times of slow growth and inflation – for example consumer staples, healthcare and the luxury sector – all the companies that will be able to protect their margins.

Ultimately - as we know - investing is key to building long-term wealth. Think about purpose and investing in a sustainable manner: it’s about time in the market, not timing the market. Investing is for the long term – we are not timing the market, not trying to buy at the right time, sell at the right time, but instead, the goal is to keep investing.

Summary of the session

1/ Macroeconomic outlook

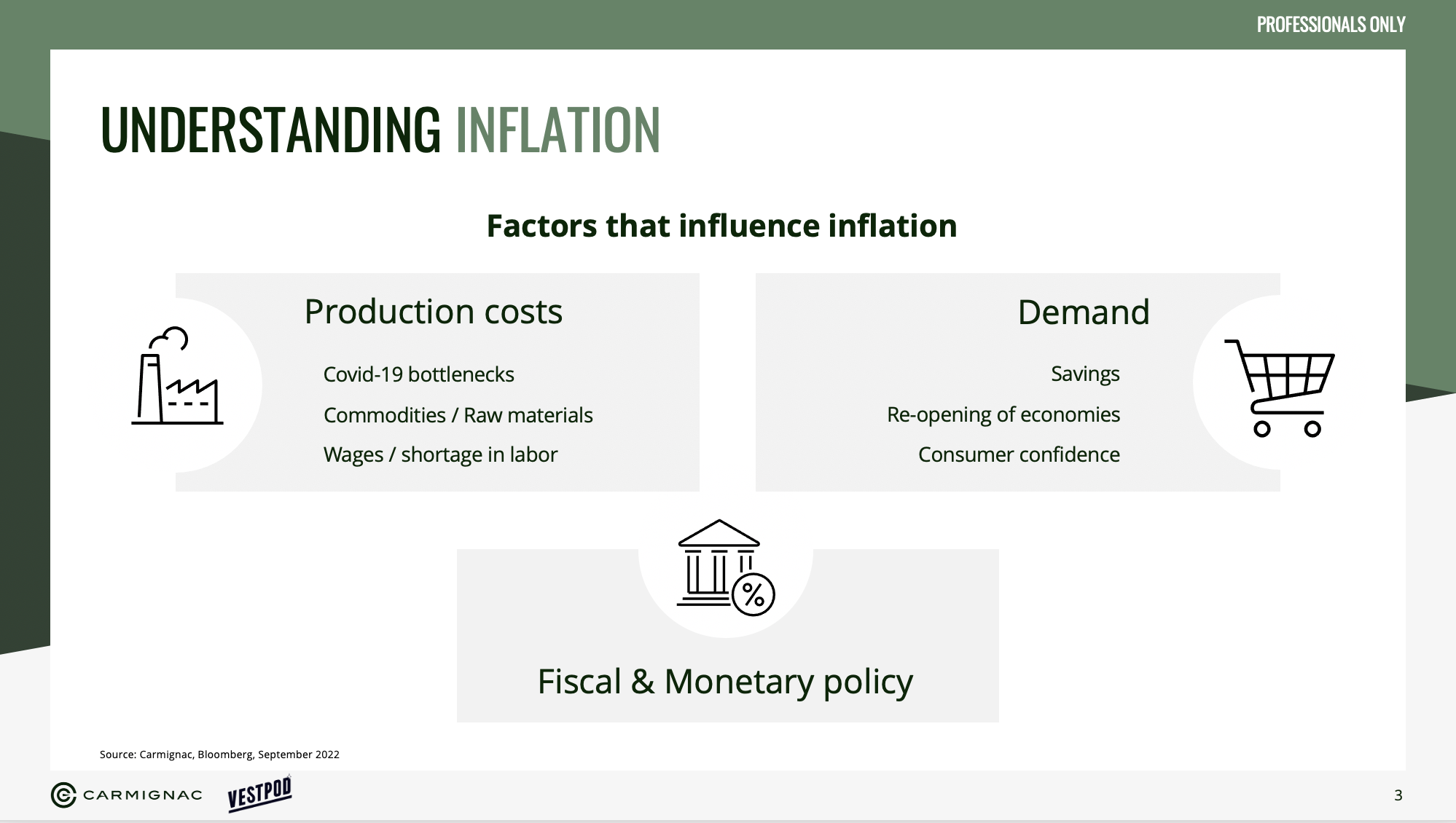

Inflation

The primary concern of investors and households is inflation – which can be defined as “the loss of purchasing power over time” - and is influenced by the following factors: production costs, demand, and fiscal and military policy.

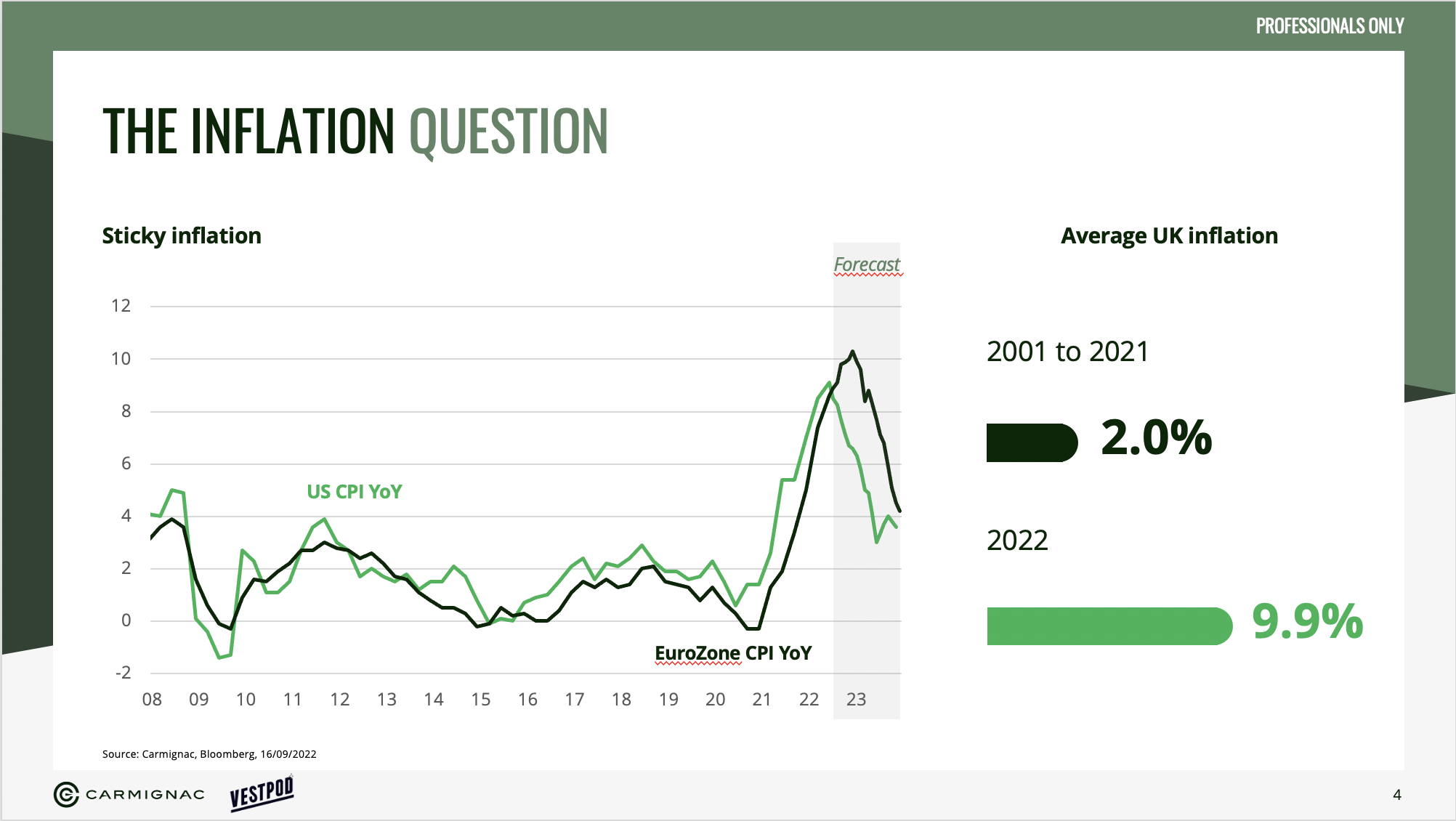

Over the last decade or two, we’ve had very low inflation (below 2%) - whereas, in the year to date, we’ve had almost 9% in the US, and almost 10% in the UK, with the same pattern across all the developed economies. Inflation may have peaked in the US, it should peak in Europe by the end of the year.

The key issue: inflation is likely to remain well above what we had over the last ten years for several more months (and maybe even several more years). What led to this situation of super high inflation was initially presumed to be a short, post-pandemic transition; in reality - it has stretched on.

Over the last months, factors fueling inflation have accumulated massively leading to a massive snowball effect. The inflationary pressures started in 2021 with the reopening of economies post Covid that has resulted in a faster rebound in demand than in supply in many sectors. Indeed, after the Covid, supply has been constrained by several bottlenecks like shortage of semiconductors, or saturation of transport capacities. Labor shortages in many industries, once again post covid, have led wages to go up which has been the starting point of a wage/price spiral. The surge in commodity prices has added to all these factors.

After injecting money into the system for almost 15 years to boost inflation, central banks are seeing the ‘ketchup-bottle’ effect - like when you shake a ketchup bottle, and first, there’s a little and then suddenly way too much. With the Central Bank, they have kept shaking the bottle (ie injecting money), but no ketchup came out(i.e. inflation) . So they shook it even harder – and at the end, the ketchup came out in an inflationary rush.

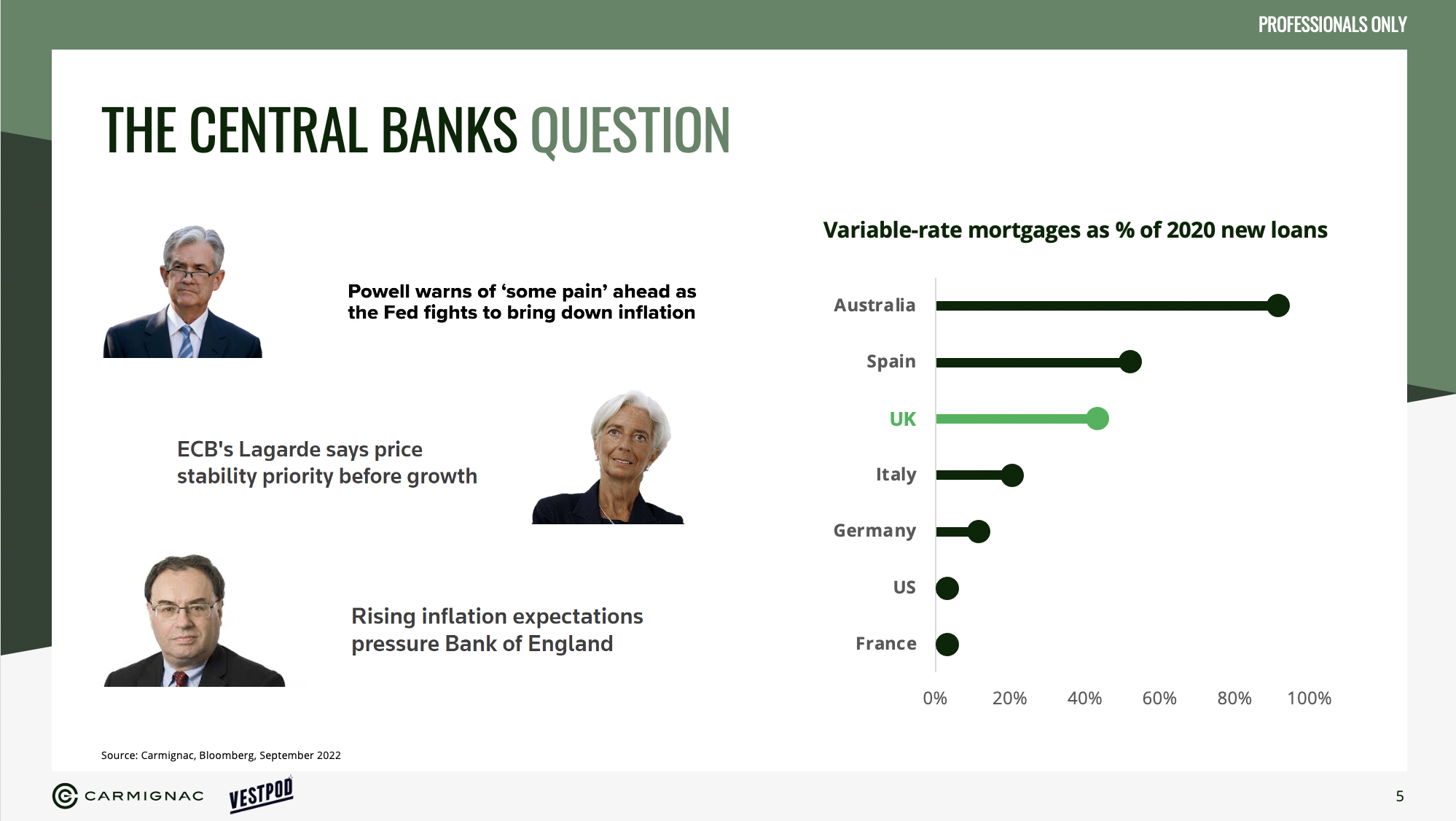

Central banks

All the central banks have pretty much the same mandate. If we take the example of the US central bank, it has a dual mandate – pursuing the economic goals of price stability and maximum employment. Therefore the target of inflation is at 2% over the long run to meet its mandates. However, currently inflation is almost at 9% in the US prompting all central banks to act very quickly to stop this price spiral. Right now, they’re willing to bring down inflation even if it hurts growth - because inflation effects are harmful for households, companies and governments.

Central banks are doing everything to tackle inflation, and a key tool they're using is the famous policy rate. With this policy rate, they can definitely influence the interest rate and therefore reduce demand. A higher rate will automatically slow the economy because the cost of loans will grow higher, resulting in consumers and businesses borrowing less and therefore consuming less.

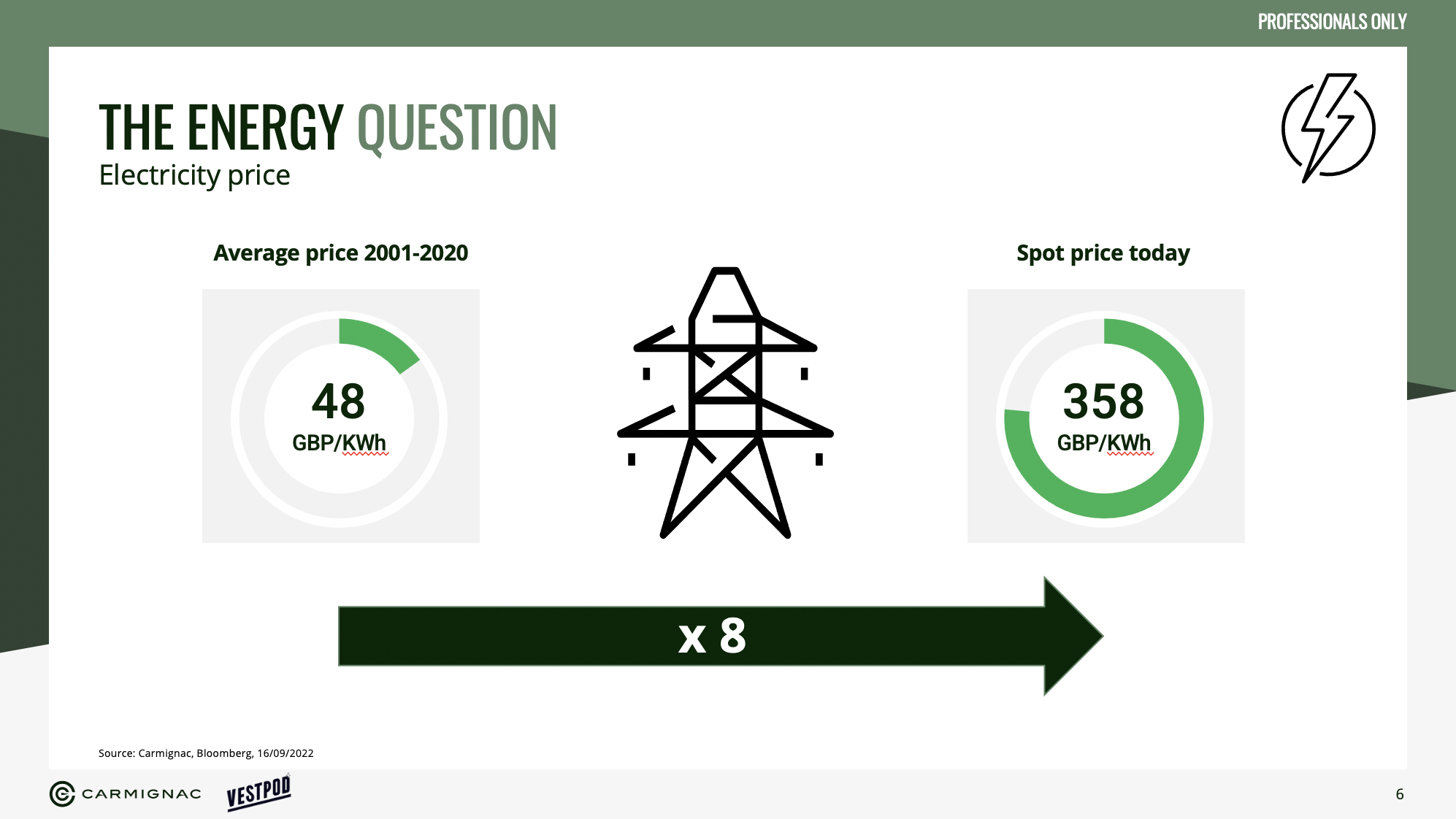

Gas situation

European gas prices are now 10 times higher than the average level of the past decade. This energy crisis that is impacting oil, gas and the electricity market started before the Russia-Ukrainian conflict – it started with the COVID-19 pandemic and follows the same patterns of bottlenecks.

While the UK is not very dependent on Russia, the UK is facing some of the highest prices in Europe, as the country relies more heavily on gas than most of the European countries and has an energy mix that is quite different with less nuclear, less renewable energy and more gas. The UK is also suffering from the fact that there is not much capacity to store gas, forcing them to buy a lot on the short-term market, where there is great volatility in prices.

2/ Market Outlook

A review of the year to date

It has been a very complicated start of the year for equity markets because inflation + tightening central bank + slowdown in growth = one of the worst cocktails ever for the market. We have alternated between inflation scares and the complete opposite. Saying all that, some sectors are more resilient than others - such as healthcare.

Market outlook

The market is very unpredictable, and no one can know what's going to happen. However, we know that markets will look at two key factors: companies’ earnings and central bank actions. Any slowdown in GDP growth will weigh on company earnings and therefore on equity markets. Equity markets are somehow ignoring the impact of a potential growth slowdown that is created by inflation, central bank actions and energy crisis.

Some sectors are more resilient to this environment. Healthcare and staples are generally perceived as defensive by markets participants. But more surprisingly it is also the case of luxury brands that tend be insulated in an economic slowdown because most of the sales come from the super wealthy that are less impacted by crisis.

A note about tech

Investing in tech will be quite different in the future than it was over the last 10 years – previously, a low-interest rate environment and liquidity have pushed a lot of tech companies to get easy access to money. So we will need to be more selective in tech investments.

At the same time, we are moving into a world of digital transformation, and this could be just the beginning of a huge structural change. For example – today, only ten per cent of business spending has moved to the cloud, and this figure is expected to triple by 2025.

Remember the golden rule: equity investment is all about time, not timing

It’s about diversifying your savings across asset classes, across companies, across sectors, across countries – and having a long-term investment horizon. It’s not just about short-term returns – we are here for a long time; companies are here for a long time. You have to be patient.

Outstanding question asked during the webinar:

What are your thoughts on the real estate market?

Axelle is not a real estate expert, but here she has a look at some of the key factors that drive the real estate market, namely growth and interest rate.

Growth momentum: massive fiscal stimulus should help dampen the recession, but we do expect negative growth for Q4-2022 and Q1-2023. If the fiscal stimulus is likely to tame inflation over the short term, it will not solve the issue of inflation over the medium term; indeed, lesser contraction in activity, given the very tight labour market, means that second-round effects are even more likely to materialise. So basically, lower energy inflation over the short term but more domestic (driven by wages) inflation over the medium term.

Interest rates momentum: BoE, the UK central bank, has already aggressively raised rates and should be even more aggressive in its tightening process in order to bring down inflation at all costs. The BoE is even more under pressure after the announcement of a package of tax cuts. As the pound tumbled to a record low and government bonds are attacked by markets post the announcement, the Central bank may be forced to increase the rate even more than initially expected. Markets currently think that BoE will increase rates as high as 6%. Indeed, fiscal profligacy is no longer in order. Markets and Central Banks are no longer playing ball due to the inflation environment => bound for higher rates and no rules for fiscal accommodation.

This higher level of central bank interest rates will have an impact on mortgage rates and on the real estate market as the UK has a high level of variable rates mortgage vs the rest of Europe, which could create some instability in the real estate market.

Overall, the current macroeconomic environment could weigh on the real estate market. However, like for any other investment, it is important to keep a long-term investment horizon to smooth out shocks and diversify savings across assets.

💖 I wanted to say a massive thank you to our speaker Axelle, you were brilliant! As well as our partners Carmignac.

I highly recommend you to listen to the episode we recorded with Maxime Carmignac a few weeks ago here and join us for our next quarterly update.

Carmignac is an independent asset management firm established in 1989 on three core principles that still stand true today: entrepreneurial spirit, human-driven insight and active commitment. We are as entrepreneurial today as we have always been; our team of fund managers keeping the freedom and courage to perform independent risk analysis, translate it into strong convictions and implement them. Our collaborative culture of debate, on-the-ground work and in-house research means we will always enhance data analysis with human-driven insight to better manage complexity and evaluate hidden risks.

We are both active managers and active partners, committed to our clients, providing transparency on our investment decisions and always be accountable for them. With a capital entirely held by the family and staff, Carmignac is now one of Europe’s leading asset managers, operating from 7 different offices. Today, as throughout our history, we are committed to try harder and better to actively manage our clients’ savings over the long-term.